Historical Perspective

Current price/share is 111,045 $. Thus the discount is 18%

Warren Buffett has led Berkshire Hathaway since 1965. In that period of 45 years, Warren has grown the book value of the firm by 20.2%. Market value of Berkshire has grown at close to book value. Over the last 20 years, Berkshire book value has grown by 22.25 times – an annual compounding of 16.8%. The market value has grown by 16.42 times – an annual compounding of 15%. How many companies or fund managers can match that.

Opportunity

The above also brings us to the opportunity in Berkshire. For the longest period, Berkshire was way over the book value because of Buffett premium. Over the last 20 years that premium has shrunk. This coupled with a few one-off events like Underwriting losses (expected) in 2011, Sokol-gate and market idiosyncrasies now provides us some fantastic opportunity to start a position in Berkshire. Below are 2 ways to value Berkshire.Approach 1

Current price/share is 111,045 $. Thus the discount is 22%

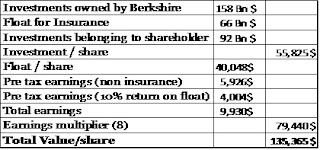

Assumptions:· Above approach counts the $66 Bn of float as part of investments/share with the expectation that the float will remain stable over the years (ideally, it will grow).

· I have used pre-tax earnings multiplier of 8 for Berkshire vs 10.5 for S&P 500 (PE is around 15 for S&P 500. Assuming 30% tax rate, pre-tax earnings multiplier is 10.5).

Approach 2

Current price/share is 111,045 $. Thus the discount is 18%

Assumptions:

· Exclude the $66 Bn of float as part of investments/share.

· Assume 10% return on the float (vs more than 20% ROI that Warren has produced during his career).

· We are not accounting for any growth in float over time.

· I have used pre-tax earnings multiplier of 8 for Berkshire vs 10.5 for S&P 500 (PE is around 15 for S&P 500. Assuming 30% tax rate, pre-tax earnings multiplier is 10.5).

Summary

With very conservative assumptions above for both approaches 1 and 2, we still get a discount of 20% for Berkshire. Thus we have a small margin of safety for Berkshire investment. Now let us look at the qualitative factors for Berkshire.

Qualitative Factors

Qualitative factors are a key ingredient to how the investment works out in the long term. Some of the key ones that I consider are:

· Management: This is one of the best aspects about Berkshire. Warren has been running Berkshire for 45 years and he is the best management-owner one can hope to get. He always considers the return on investment before making any investment. He judges himself by that yardstick and that is one of the reason Berkshire has done so well.

· Culture: Berkshire culture is very long term oriented. This allows them to be patient when markets are not favorable. This allows them to make logical decisions without getting pressured into what the street is thinking or what their competitors are doing.

· Unique businesses: Berkshire has collected an eclectic mix of businesses that have unique competitive advantages. This allows them to handle down markets relatively well. It also allows the businesses not to be as impacted by the market competition thus preserving profitability.

Conclusion

· Berkshire is currently trading at 20% below the intrinsic value.

· Berkshire has the some of the best qualitative factors. This allows the investor to be very comfortable and not have to worry about short term improvements.

· This is a phenomenal opportunity to invest in one of the best businesses available and where the business is selling at a discount with very limited downside risk.

Disclosure: Long Berkshire. Looking to increase position on dips.

The same article was also posted on Gurufocus website and generated some very good comments.

ReplyDeletehttp://www.gurufocus.com/news/136190/berkshire-hathaway--a-good-opportunity

So for those of us who can't afford the class A's, would you attribute the same opportunity to the class B shares?

ReplyDeleteJust read you entire blog dating back to 2009. Would be interested to know what your position is with SLT and ACTS as both have dropped significantly since the end of 2009, when you last spoke of them. ACTS looks to be down 25% from it's high that you posted and SLT closer to 30% although it is still well over 100% returns from your buy price. Any update on your positions with those.

Hello David

ReplyDeleteI have kept my ACTS position intact. Haven't sold any since Feb 2009. So it has gone up and down. I will continue to monitor the progress and then make decision on selling.

On SLT, I sold a portion 1/5 in between last year (I think). I am keeping the remaining since I expect significant growth in earnings in 2011-12 as power plants start coming online. However, I am mindful of the commodity cycle so watching it carefully.